The dilemma between protection and utilization

- Corporates are committing large amounts of financing for forest protection and restoration;

- The increasing number of urban dwellers, mainly in developing countries, will drive timber consumption to unseen levels in the next decades;

- Existing forests and plantations are unlikely to feed the insatiable appetite for timber, which ratifies the need for an increase in sustainably managed forest areas and value chains;

- Private sector investment into sustainable forest management in emerging economies is needed and innovative financing mechanisms are required to meet this challenge.

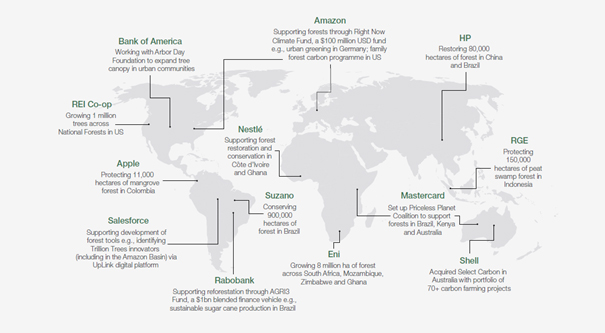

Corporate investments in forests are in vogue. Not a single week goes by without announcements of significant financing commitments for forest protection and forest restoration1. When following the media, one could conclude forests are the panacea against climate change and the biodiversity crisis. Protecting and restoring forests to secure the future of mankind is at the top of corporate and political agendas, expedited by increasing demand in high quality carbon credits, a large share generated through forestry projects. Prices for forest related carbon from nature-based solution projects are outpacing the price development of reduction credits, such as renewable energy2. Corporates and governments are seeking to achieve net zero commitments3. Figure 1 illustrates a sample of corporate pledges on forest conservation and restoration.

Aside from the environmental benefits, forests also deliver highly coveted and valuable raw materials. Which leaves us with the question: Can we – from a market perspective – afford to protect all the forests?

Wood consumption – the demand side

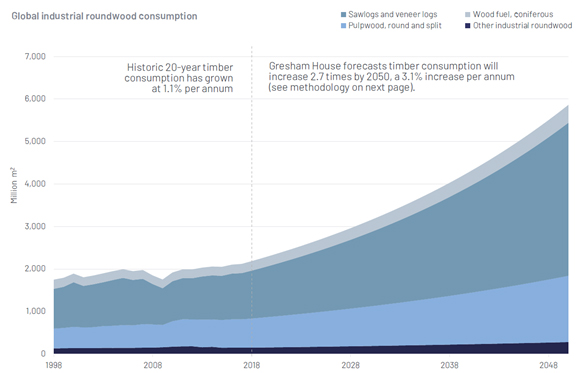

Consumers often don’t realize how omnipresent wood as a raw material is and how dependent their lives on wood products are. Figure 2 illustrates the global timber demand forecast, split into different assortments. With increasing wealth timber consumption per capita will follow – not for firewood, but for high quality and processed wood products. For instance, wood used for sustainable housing, furniture or tissue will experience an upswing in demand through prosperity increases in many emerging economies. Timber can be considered the most climate friendly construction material. The highest consumption is seen in assortments used for timber construction, which is driven by a rising number of urban dwellers. In 2018, global industrial roundwood consumption was approximately 2.2 billion metric cubic meters, which are roughly 65 million truckloads or 2,200 times the volume of the Empire State building. Taking population growth, increase in wealth and similar timber consumption rates of industrialized countries, wood demand is projected to climb up to almost 6 billion metric cubic meters annually by 20505. Against this backdrop, the question is not about protecting all our forests, but rather how will our forests survive this insatiable appetite for timber?

Timber harvesting – the supply side

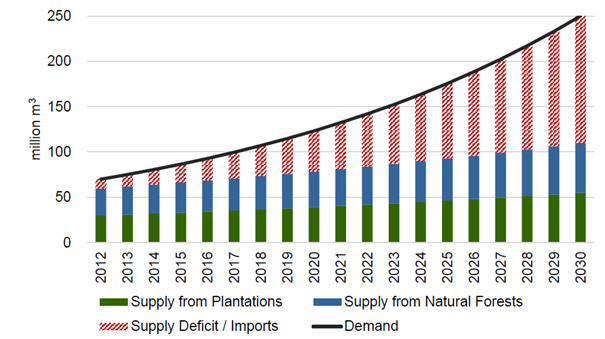

To answer this question, we need to investigate where and how timber is grown. On a global scale, the wood market is balanced and there are almost no reserves of harvested logs, as timber is only harvested after having been sold6. Having said this, when looking into different timber streams and continents the picture becomes blurry. Forest levels in developed countries have been stable for many years. Sustainable management practices, combined with protected areas dominate the landscape7. But what’s the situation in emerging markets? Taking Africa as an example, Figure 3 visualizes the historical and projected wood consumption and supply. African undersupply is clearly persistent, turning into a major threat for forests. Wood is desperately needed, and to protect the forests it can only come with sustainable practices8. In Latin America sustainable forestry practices have been experiencing an upwards trend, in Africa and South East Asia sustainable forest management is catching on at a significantly slower rate.

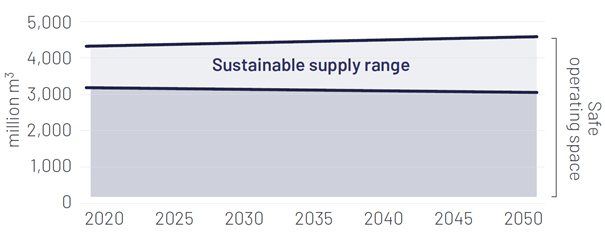

A continued increase in demand of wood products over the next two decades is inevitable. Hence, overseeing this development and refusing to increase timber production is burying our heads in the sand. Figure 4 puts the supply deficit into perspective as it illustrates the maximum harvesting level under a “safe operating space”. Up to 2030 the world’s forests will most likely meet demand, but going forward the supply deficit will strike, in some regions this will happen earlier, (or is already the case as we saw in Africa).

Getting out of the dilemma

The goal must be to establish sustainable forest and value chain management globally. Forests, if managed the right way at the right location, can supply us with the sustainable product par excellence. The growth in timber demand needs to go hand in hand with increased measures of protecting and restoring forests for climate change mitigation, as well as protecting our remaining primary forests for safeguarding biodiversity. Nonetheless, there are limited options to increase the amount of sustainably produced wood. Through mobilization of unused stock a slight upside in harvesting levels globally can be realized, but not sufficient to meet the increasing demand. The challenge is to increase the productive forest area on one hand, to meet the timber demand and protect and restore more forests and degraded land on the other. This is where the financial sector comes into play, as establishing forests and plantations is a cost-intensive exercise.

Only large-scale private sector investment can address this financing need. There are innovative approaches, such as the new partnership recently announced at COP26 between CDC Group, Finnfund and Norfund to partner with New Forests to raise USD 500m for sustainable forestry across sub-Saharan Africa12.

A mechanism FS Impact Finance is managing together with UN Environment is the Restoration Seed Capital Facility (RSCF), which is enabling sustainable land use investments in the forest landscape restoration sphere through different support mechanisms. RSCF is offering a support line for fund establishment, to increase the number of investment vehicles in the market, and is supporting existing funds through pipeline and project development support to overcome the scarcity in investable projects in the sector. Get in touch with the RSCF Team to find out more!

More on the topic will be published in following blog articles about sustainable forest management and financing this transformation.

Footnotes

1 https://ukcop26.org/the-global-forest-finance-pledge/

2 Ecosystem Marketplace insights report: State of the voluntary carbon markets 2021

3 https://unfccc.int/climate-action/race-to-zero-campaign

4 World Economic Forum: Investing in Forests: The Business Case 2021

5 Gresham House: Global Timber Outlook 2020

6 Gresham House: Global Timber Outlook 2020

7 or with an off-taking agreement in place

8 FAO: The state of the world’s forests 2020

9 FAO: The state of the world’s forests 2020

10 Allocating Capital for Maximum Impact in Africa’s Plantation Forestry Sector 2017; data has been adjusted to supply and demand of integrated pulp producers in South Africa

11 Gresham House: Global Timber Outlook 2020

12 https://newforests.com.au/cdc-group-finnfund-norfund-propose-innovative-partnership-with-new-forests-with-an-ambition-to-raise-500m-for-sustainable-forestry-across-sub-saharan-africa/